The core principle I operate by in the markets is that there is no single superior system or approach. The best and most robust results come from combining different trading styles.

This may sound obvious, but traders without practical experience often do not understand the power of combining systems that share the same capital pool. Many traders assume that adding an intraday strategy - like the live Volatility Breakout system I track daily here - means they have to liquidate their core swing positions or drastically increase their account size to handle the margin requirements.

Today, I want to share a practical lesson on portfolio construction, capital efficiency, and why the math actually favors combining these two styles - even on a smaller account.

The Baseline: Core Swing Portfolio

Let’s say you are building a systematic portfolio with a smaller account, perhaps around $15,000. You might start with a few foundational swing systems. Let's use the ones I have described on this site and track on a daily basis. It is important to note that I have traded these live for several years - this post does not cherry-pick an arbitrary backtest that merely looks good on paper, but rather reflects real, out-of-sample reality.

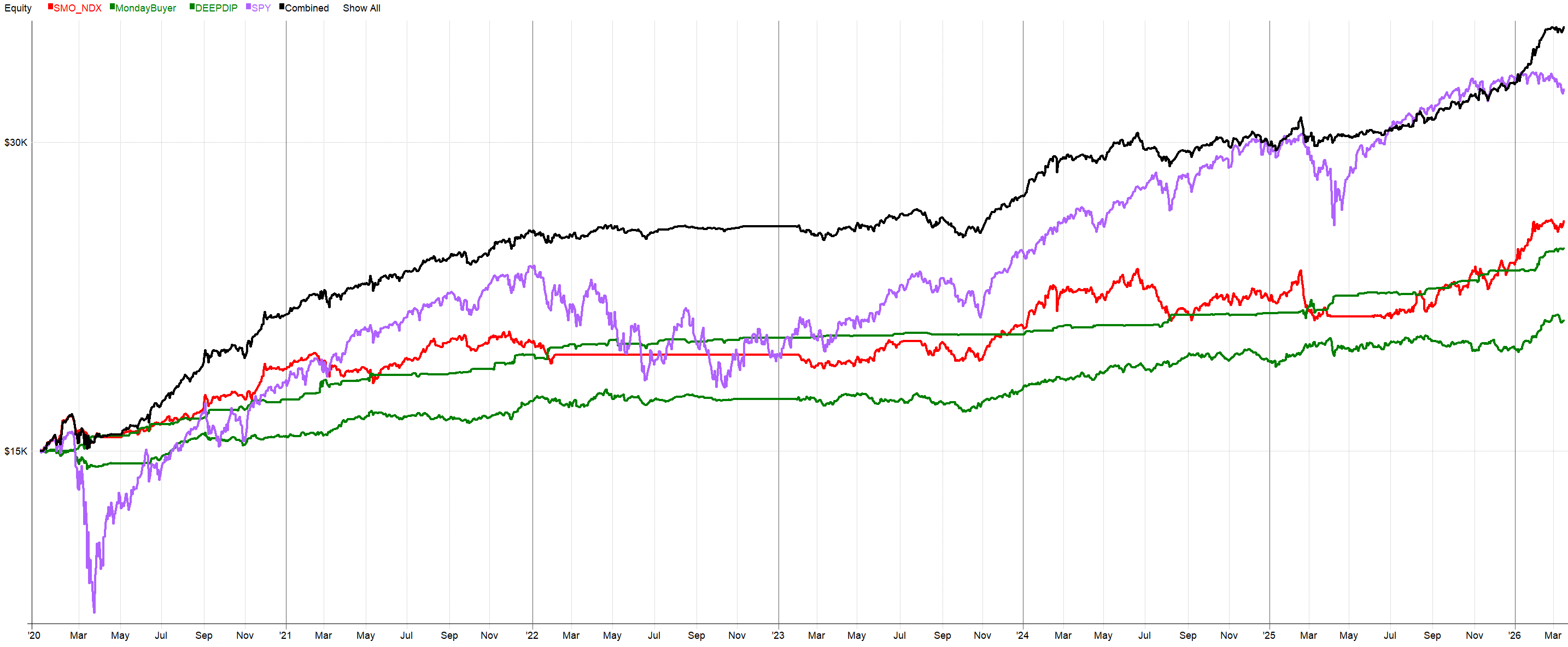

These are the components of our baseline portfolio:

- NDX Momentum: A relative momentum strategy trading Nasdaq 100 stocks using volatility targeting. I have been trading the same version of this strategy for many years.

- Buy the dip (weekly): A slower mean-reversion strategy that involves buying stocks from the S&P 500 index into longer-term trends.

- Deep Dip: A fast, short-term mean reversion strategy that leverages implied option volatility for precise entry.

This is the typical structure I like to use in my core portfolios. I view systems like NDX Momentum and Buy the dip (weekly) as "smart beta" strategies - they generally make money when the broader markets rise. This is intentional. The more "alpha" (complex market timing) a strategy tries to use, the higher the chance it breaks in the future. Therefore, I build my foundation with highly robust strategies that might not independently beat the market every year, but are incredibly hard to break. Then, I add overlays with a more unique edge to boost performance.

Understanding Capital Utilization

Let's pause on the topic of overlays for a moment. Strategy sizing is based on the capital allocated to it. For example, NDX Momentum opens up to 5 positions. If we assign it $15,000 of capital, it allocates up to $3,000 per position.

Most traders assume that if we have two strategies on a $15,000 account, and we assign $15,000 for sizing to each, we will max out our capital utilization and constantly use 2x leverage. However, this is not true. These strategies do not have all their positions open at all times. Faster strategies, in particular, only trade occasionally.

Let's look at this practically. We will use the three mentioned swing strategies - NDX Momentum, Buy the dip (weekly), and Deep Dip - assigning 33% of the portfolio capital to each. If our total account capital is $15,000, each strategy will base its sizing on $5,000. In this scenario, we will logically never come close to utilizing margin leverage. The average capital utilization will only be 42%.

This means we could easily add more strategies to the portfolio and trade without heavily relying on margin.

Let's stick with our three swing strategies for now. If we look at their combined backtest versus a buy-and-hold approach on the S&P 500, even after factoring in commissions and slippage, the strategy's performance keeps pace with S&P 500 returns but with significantly lower risk and shallower drawdowns. It produces a CAGR of 16.61% and a maximum drawdown of -7.5%:

But the most crucial takeaway is that capital utilization averages only 42%. In reality, we have a "second half" of our capital sitting idle, which we can use to improve overall performance without exposing ourselves to heavy leverage.

A Crucial Note on Commissions for Small Accounts

Before adding more systems to a $15,000 account, we have to talk about execution costs. When you trade multiple systems, your position sizes per trade shrink. If you are using Interactive Brokers' "Fixed" commission structure, you will hit a major drag on your portfolio: the $1.00 minimum fee per trade. On smaller share quantities, that $1.00 minimum eats up a disproportionate amount of your edge. Furthermore, the Fixed structure offers no rebates for adding liquidity via limit orders. For systematic traders with smaller accounts, the "Tiered" commission structure is almost always superior.

In my modeling, I apply tiered commissions, which calculate roughly to $0.0035 per share with a much lower minimum of just $0.35. I also build in a realistic slippage of 1.5 ticks per trade—which matches the actual fill data I see in live trading. To trade multiple systems efficiently, you must get your friction costs down.

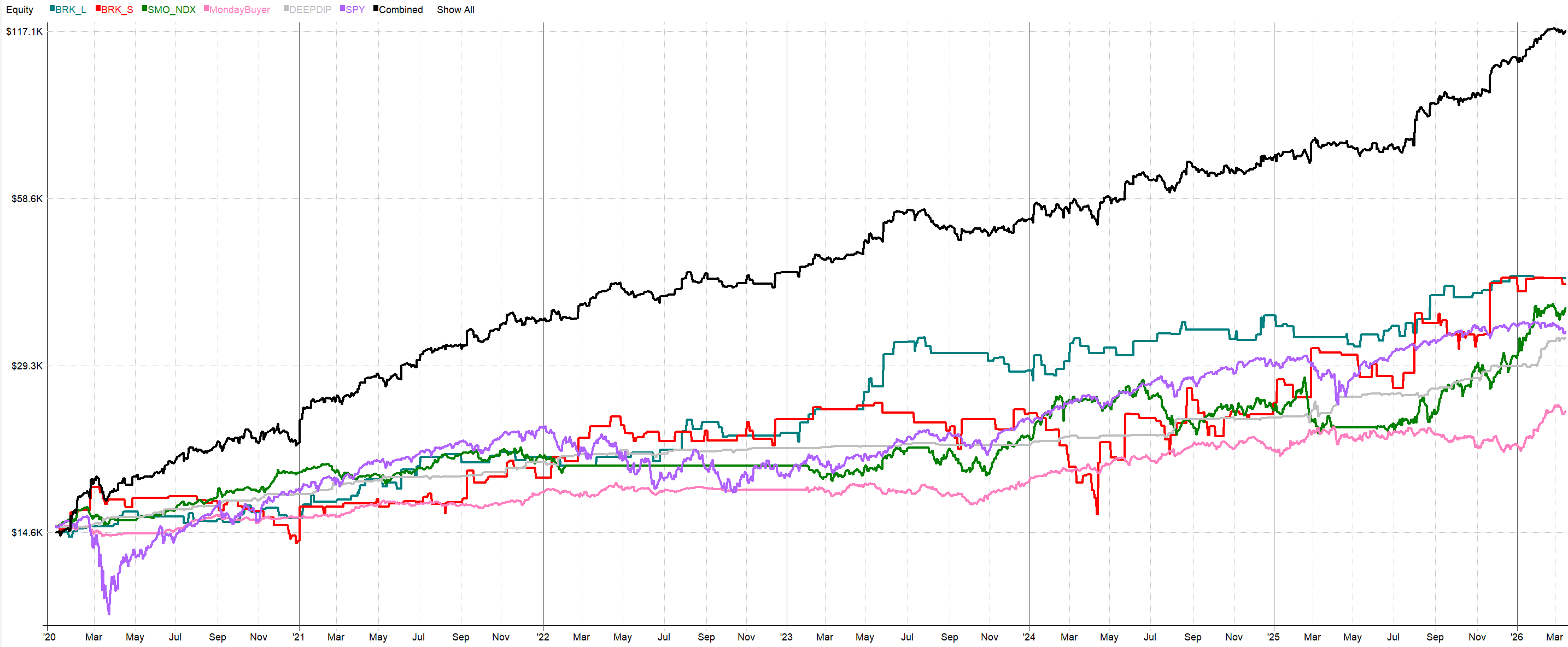

Capital-Efficient Intraday Breakouts

With tiered commissions set and nearly 60% of our capital sitting idle on an average day, we can introduce the intraday model. The realistic minimum capital for this system is $15,000 to $20,000 to trade multiple markets efficiently. However, on a $15,000 account, we can still execute the strategy comfortably by stripping it down to a single market: Micro Nasdaq (MNQ) futures, for example.

By dedicating a strict 2% risk per trade ($300 at the start with a $15,000 account), we have more than enough buffer to open the MNQ position even in a higher volatility environment. (Note: My testing framework utilizes the QQQ ETF to model this, which yields very similar results to the micro futures. The ETF results do get slightly better due to finer position sizing flexibility ).

Because the intraday system does not hold positions overnight, and a single MNQ position requires just $2,350 in margin at Interactive Brokers, it executes without ever requiring excessive leverage and cleanly stacks on top of our swing portfolio.

The Synergistic Result and Realistic Expectations

When you combine those core swing strategies with an uncorrelated intraday breakout system, the portfolio metrics shift dramatically.

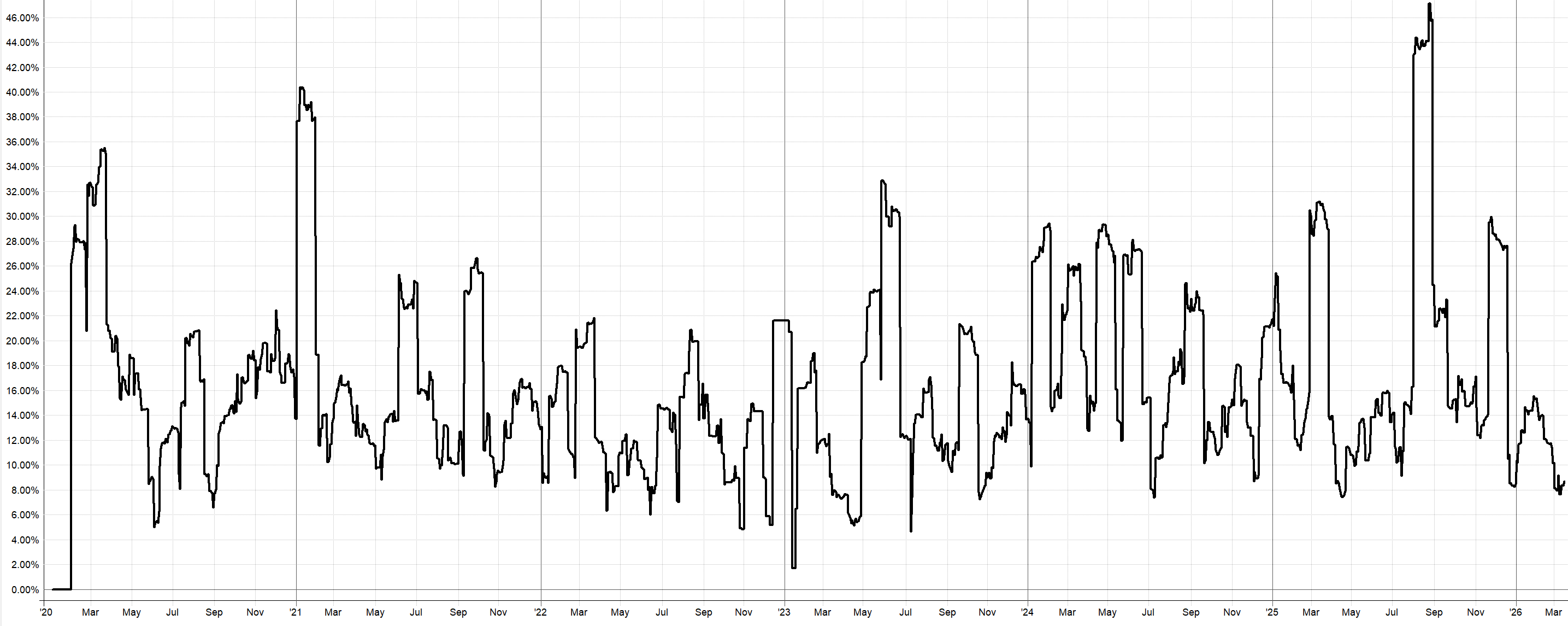

In my modeling for this combined portfolio, the addition of the intraday MNQ breakout pushed the theoretical annual return to roughly 39%, maintaining a strong Sharpe ratio of 1.83:

The annualized volatility landed at about 18%:

That 15% to 20% volatility range is exactly where I aim for a smaller account. This kind of annualized volatility will naturally create drawdowns of 20% to 25%, which should be mentally acceptable for a prepared trader.

As you can see, adding an intraday system does not create a holy grail, but it significantly increases the robustness and capital efficiency of our trading. Intraday breakouts, for example, can serve as an excellent hedge for swing strategies.

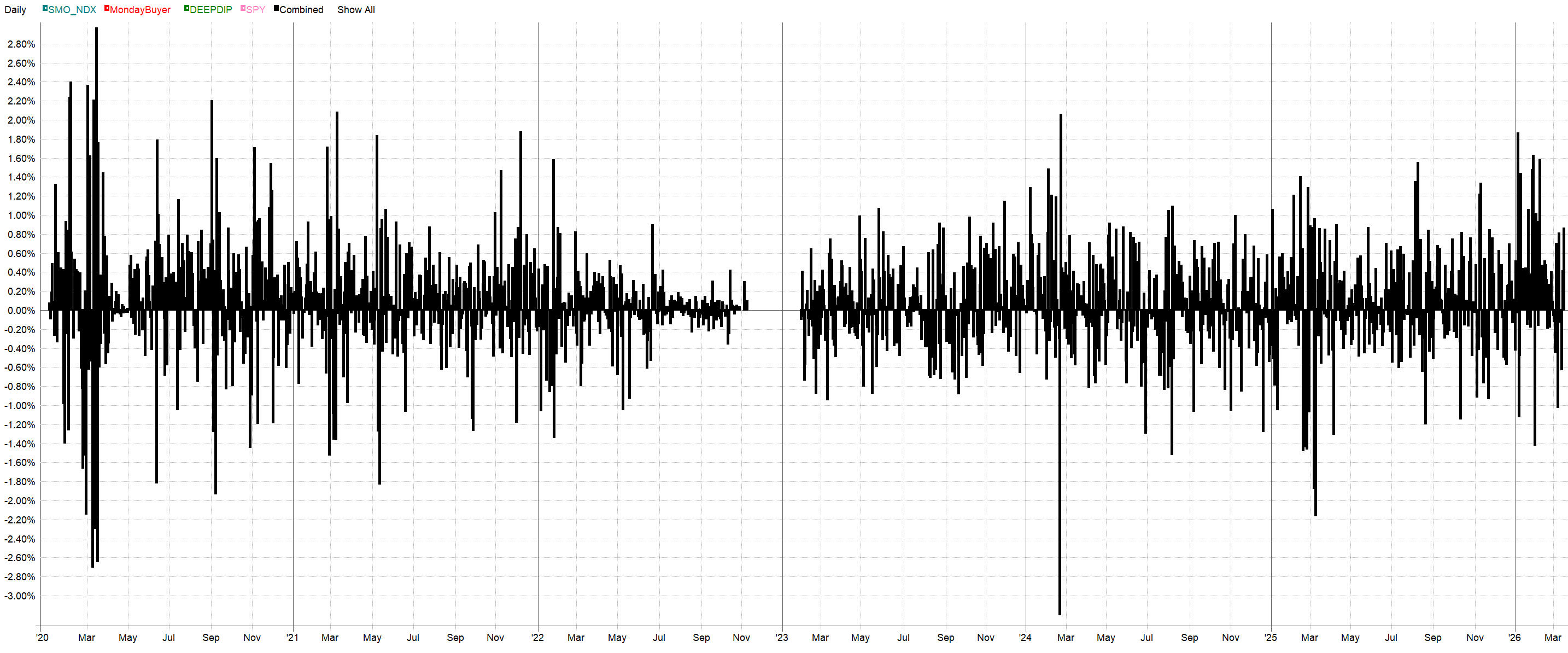

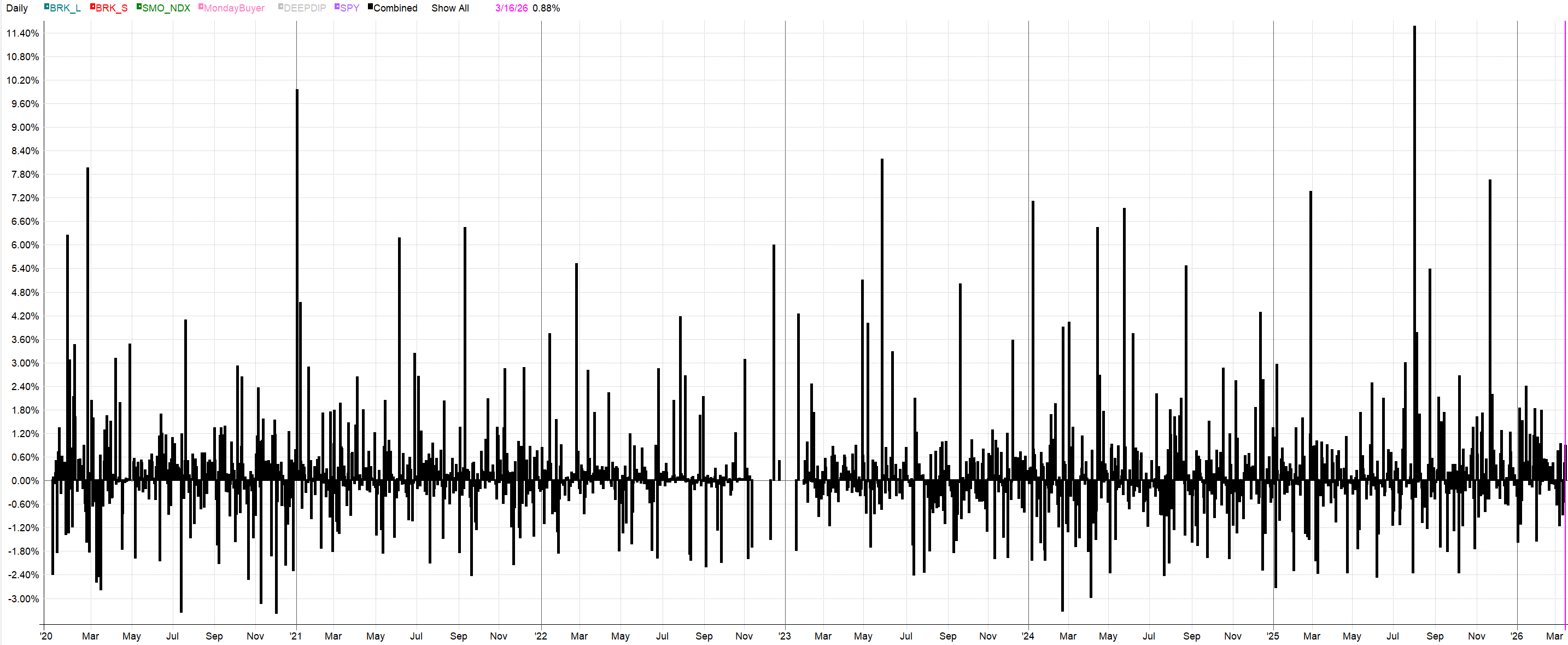

One of the key metrics I monitor in my portfolios is the distribution of daily volatility. If we look at the daily fluctuations of our standalone swing portfolio (just the three long strategies), the distribution of daily moves generally ranges from -3% to +3%:

After adding the intraday system, the maximum daily loss remains firmly capped around that -3% level, but the daily profit potential shifts into significantly higher brackets. There are now many days showing outsized gains of +6% to +10%:

This clearly demonstrates how adding a strategy with a different trading frequency and a distinct risk profile can drastically improve the characteristics and profitability of your portfolio—without requiring aggressive leverage or additional capital.

By the way, all performance metrics from May 2023 onward are genuinely out-of-sample in this test, as I have personally traded all these strategies exactly as I share them here (without making any modifications). However, it is naturally essential to understand that past performance does not guarantee the same returns in the future. What we are demonstrating here is not a guarantee of specific performance, but rather the underlying principles of how I operate in the market.

Plug Intraday Logic Into Your Own Workflow

Most of you are likely already working with swing strategies similar to the ones I used for this baseline portfolio (and if not, I will be able to help you with that on CrackingMarkets soon).

However, creating a simple yet robust intraday strategy is rarely as straightforward as building a swing model.

If you want to bypass the trial and error and simply integrate my exact intraday logic into your current portfolio, you can now leverage my implementation program. Inside, I share the exact intraday system I trade with my own capital (the same one used in today's demonstration).

It includes the complete open code and my Interactive Brokers bot tools, so you don't have to build the execution logic from scratch.

The introductory pricing ends this Friday, March 20th. Review the full system, view the daily live tracking, and get the code here.