A simple intraday volatility breakout can work surprisingly well. But in live trading, the edge is often shaped by small practical details: how we exit, how much slippage we pay, and whether we can express the same idea through ETFs, futures, or 0DTE options. In this article I share several practical tests that are helping me move the strategy toward a more robust and more tradeable implementation.

If you trade intraday breakouts, the following research may give you useful ideas.

All tests in this article are based on the intraday volatility breakout framework I described in my earlier article, From Theory to Practice: Sharing My Live Intraday Breakout System. The exact parameters may be different from what you trade, but I believe many of the conclusions are useful for similar breakout models as well.

The basic idea is simple: define a average range, wait for the market to break out of it, enter in the direction of the move, and manage the position with a small initial stop-loss and a clear exit rule.

In practice, however, the small details matter a lot. A breakout strategy can look excellent in a clean backtest. Once we include commissions, slippage, missed fills, position size, and our own psychology, the ranking of different variants can change.

That is what I want to focus on today.

Quick recap of the strategy

My intraday breakout model is intentionally simple.

At the beginning of the day, I define breakout levels using the opening price and a multiple of recent average volatility. In my own tests, I use Average True Range, or ATR, to estimate what a normal daily movement looks like.

A simplified version looks like this:

- take the daily open,

- add and subtract a chosen ATR multiple,

- place long and short breakout levels around that open,

- enter when the market breaks beyond one of those levels,

- risk a small amount,

- hold the position as long as the market keeps trending.

The logic is not complicated. The edge comes from the fact that some trading days expand strongly in one direction. On those days, a breakout entry allows us to participate early enough.

But there is one important filter.

I do not want to trade every single breakout. That would generate too many signals and too many costs. Instead, I trade the breakout only in a context where my tests indicate a higher probability of a strong intraday move.

Key idea

The system does not need to win all the time. It needs to lose small when the breakout fails and stay in the position when the market produces a real trend day.

This creates two core principles:

- exit quickly when the trade is wrong,

- stay in the trade as long as possible when the move is right.

The second point sounds easy. In live trading, it is often the hardest part.

The ideal exit: simple, robust, but not always easy to hold

When building a simple intraday breakout system, one of the most robust approaches is usually this:

one trade per market per day, usually the first valid breakout, and then hold until either the initial stop-loss is hit or the market closes.

This makes intuitive sense.

A breakout strategy makes money when it catches a strong trend day. If we exit too early, we cut off the exact trades that are supposed to pay for all the small losses.

Less activity also means lower trading costs. This is not a small detail. In my live trading, commissions can represent around 10% of gross profit. That is already close to the maximum level I am comfortable with.

So the most basic exit is:

- enter on the breakout,

- place a small initial stop-loss,

- do nothing unless the stop is hit,

- otherwise exit at the end of the day, or EOD.

This fixed version is usually very strong in testing.

The problem is psychological.

During the day, a profitable trade can move strongly in our favor and then give back a large part of the open profit. If we hold until the end of the day, we have to accept that path. It may be optimal in a backtest, but it is not always easy to follow with real money.

That is why I also test trailing stop variants.

Why a close trailing stop is usually dangerous

A trailing stop looks attractive. It protects open profit and makes the trade feel safer.

But there is a problem.

If the trailing stop is too close, normal market noise can easily push us out of the position. Then the market may continue in the original direction without us.

This is especially dangerous in an intraday breakout system because the biggest profits come from a small number of strong trend days. If we exit those days too early, we damage the most important part of the edge.

In my tests, tight trailing stops are very sensitive to the exact parameters used. A small change in the stop distance can produce a large change in the backtest. That is usually a warning sign.

A more robust approach is to start trailing only after the trade has already produced a meaningful open profit. For example:

- start with a normal initial stop-loss,

- wait until the trade reaches +2R open profit,

- only then begin trailing the stop,

- trail the stop approximately 1R behind the latest favorable high or low.

Here, 1R means the original risk of the trade. If the initial stop represents $300 of risk, then +2R means the trade is $600 in open profit. Only after that point do we start protecting the move.

This gives the trade enough room to develop before we begin managing it more actively.

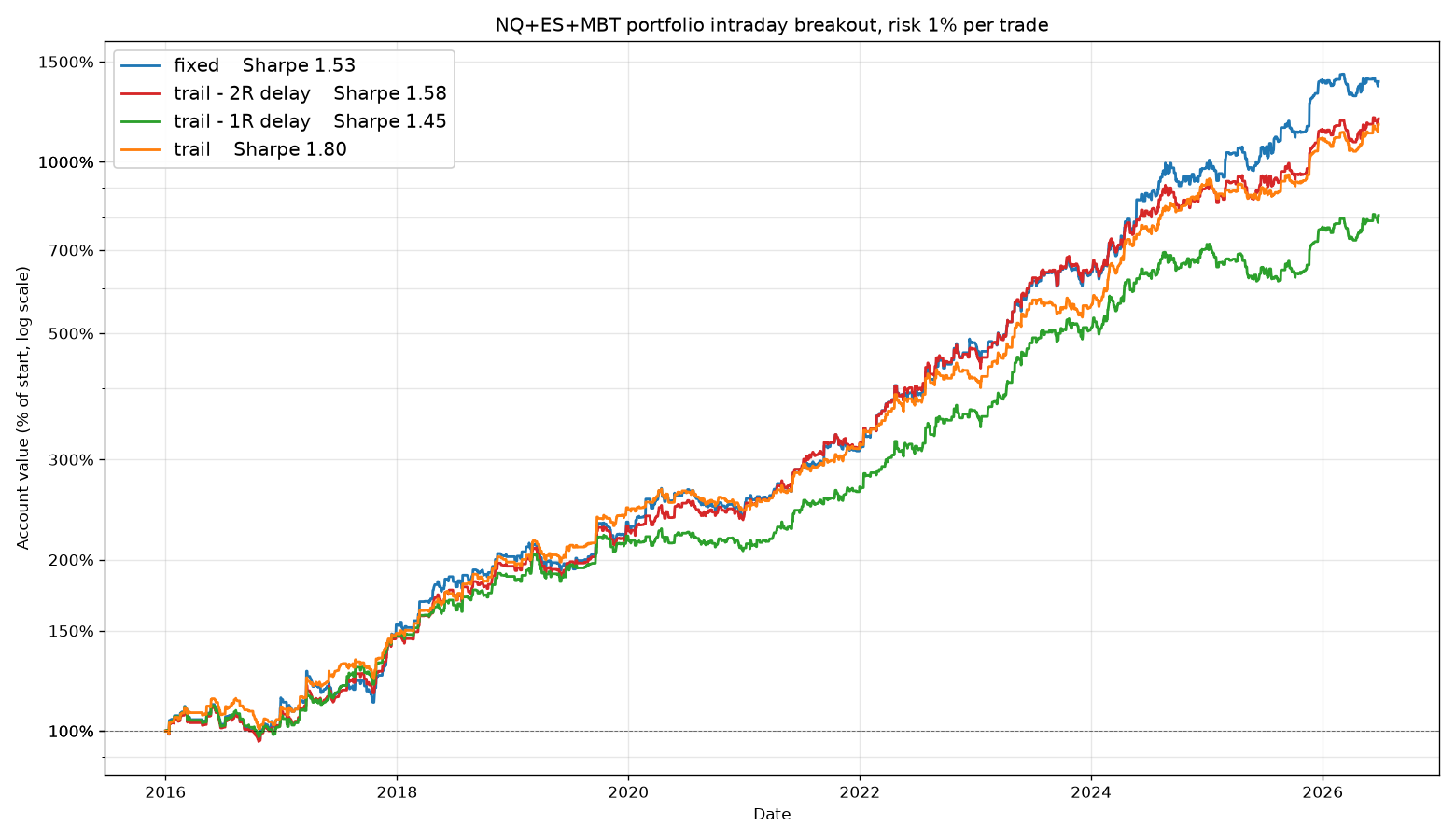

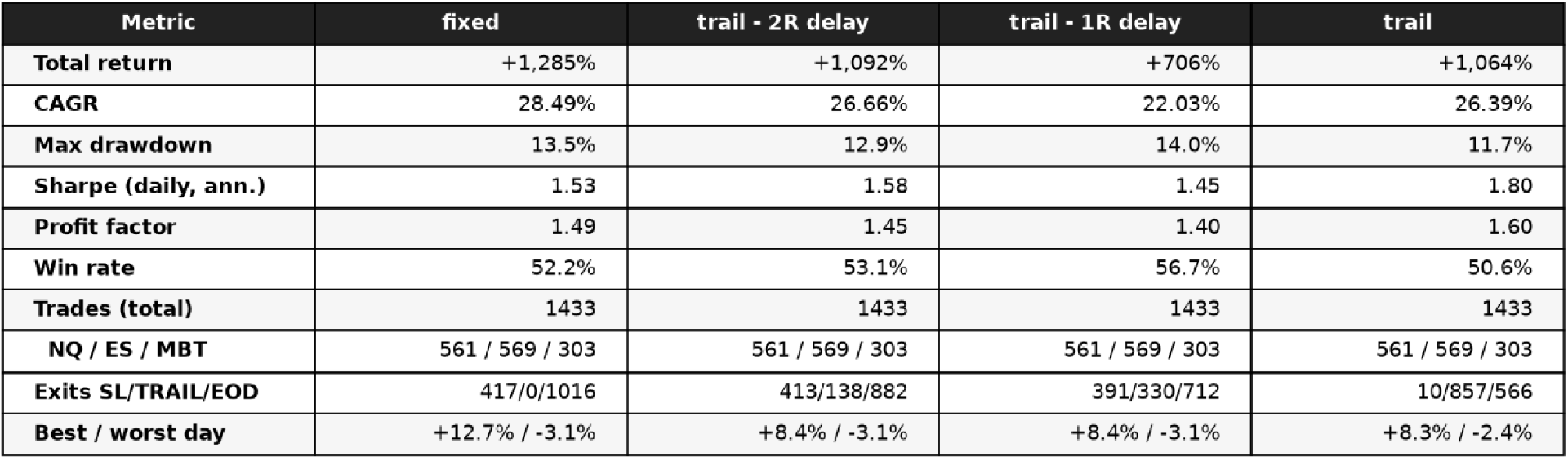

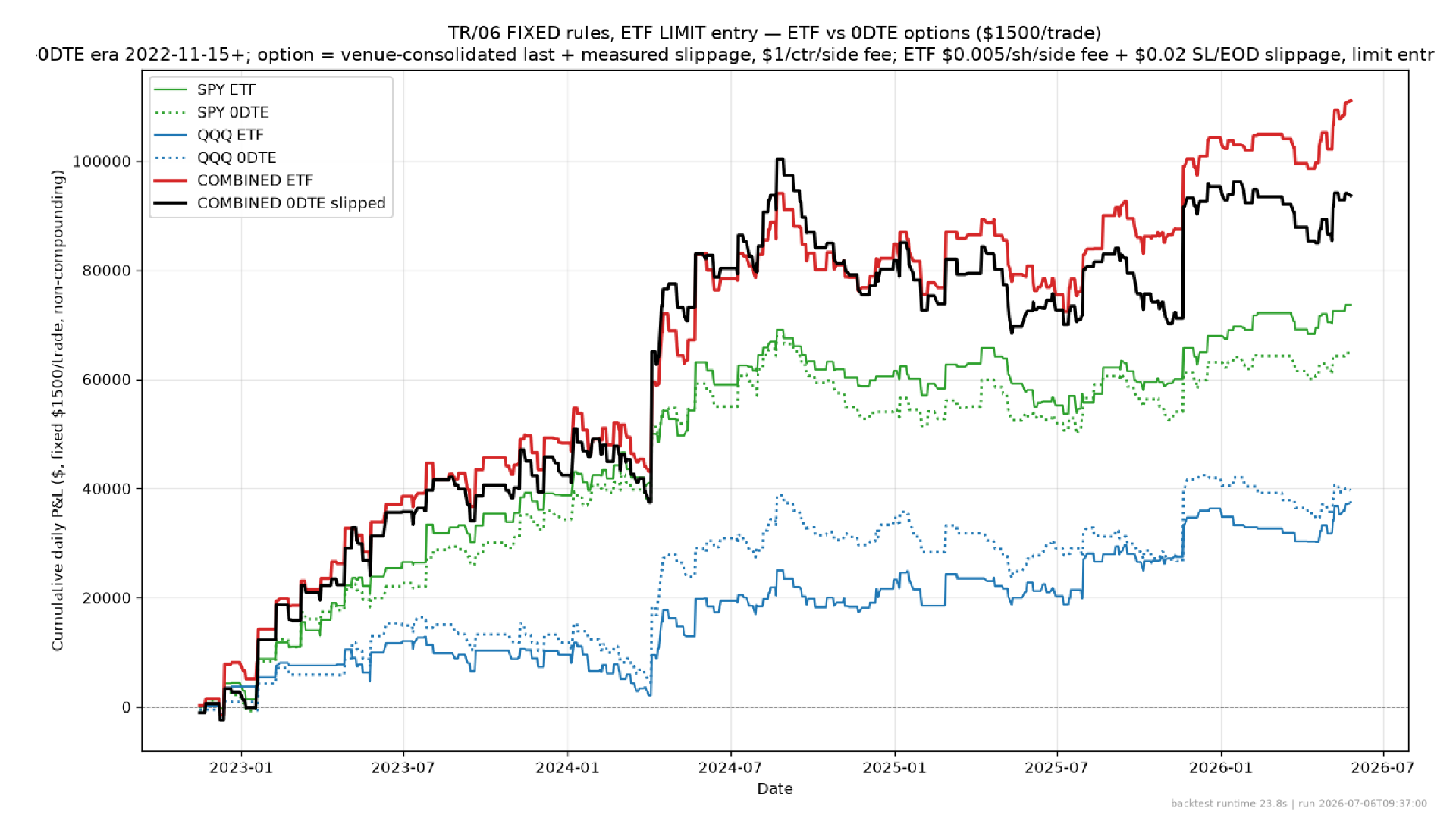

Figure 1 compares the main exit variants on a portfolio of three markets that I trade with this intraday breakout logic: NQ, ES, and MBT.

The detailed statistics show the same idea more clearly.

The fixed exit remains very attractive. It allows the system to fully benefit from the strongest intraday trends.

But the 2R delayed trailing version is also interesting. It does not beat the fixed exit in total return in this sample, but the path is similar and the trade management is easier for me to follow live.

Practical takeaway

The best backtest is not always the best live trading choice. A slightly lower-returning variant may be better if it is easier to execute consistently and less stressful to hold.

This is why I am moving more of my ETF and futures breakout trading toward the 2R delayed trailing model.

It keeps the core idea of the system intact: give trend days room to pay. At the same time, once the trade has produced a meaningful open profit, the position is no longer completely unmanaged.

For me, this becomes a better compromise as my traded size grows.

Slippage: the hidden tax in intraday trading

Intraday breakout trading can be profitable even after commissions and slippage. My own live results confirm that.

But execution matters.

A breakout entry is usually aggressive. We enter when the market is already moving. That often means we pay the spread and sometimes additional slippage.

In SPY and QQQ, my average live slippage has been below one tick per side. That is acceptable. But as position size grows, I can clearly see that the average slippage increases.

This is normal. Larger size is harder to execute cleanly, even in liquid markets.

So I started looking for a way to control execution better.

The question was simple:

Can I enter the breakout later, using a limit order, and still keep most of the edge?

Stop entry versus delayed limit entry

The standard breakout implementation uses a stop entry at the breakout level.

For example, if the long breakout level is 700.00, we place a buy stop there. When the market trades through that level, we enter.

This is simple and clean, but it usually pays slippage.

The alternative I tested is a delayed limit entry.

The logic is:

- wait for a one-minute bar to close above the long breakout level or below the short breakout level,

- on the next minute, place a limit order at the close price of that breakout bar,

- require the limit price to be penetrated by at least one tick in the backtest,

- if the order is not filled, update the limit using the next one-minute close.

This means we enter later. But we control the entry price.

That is the trade-off.

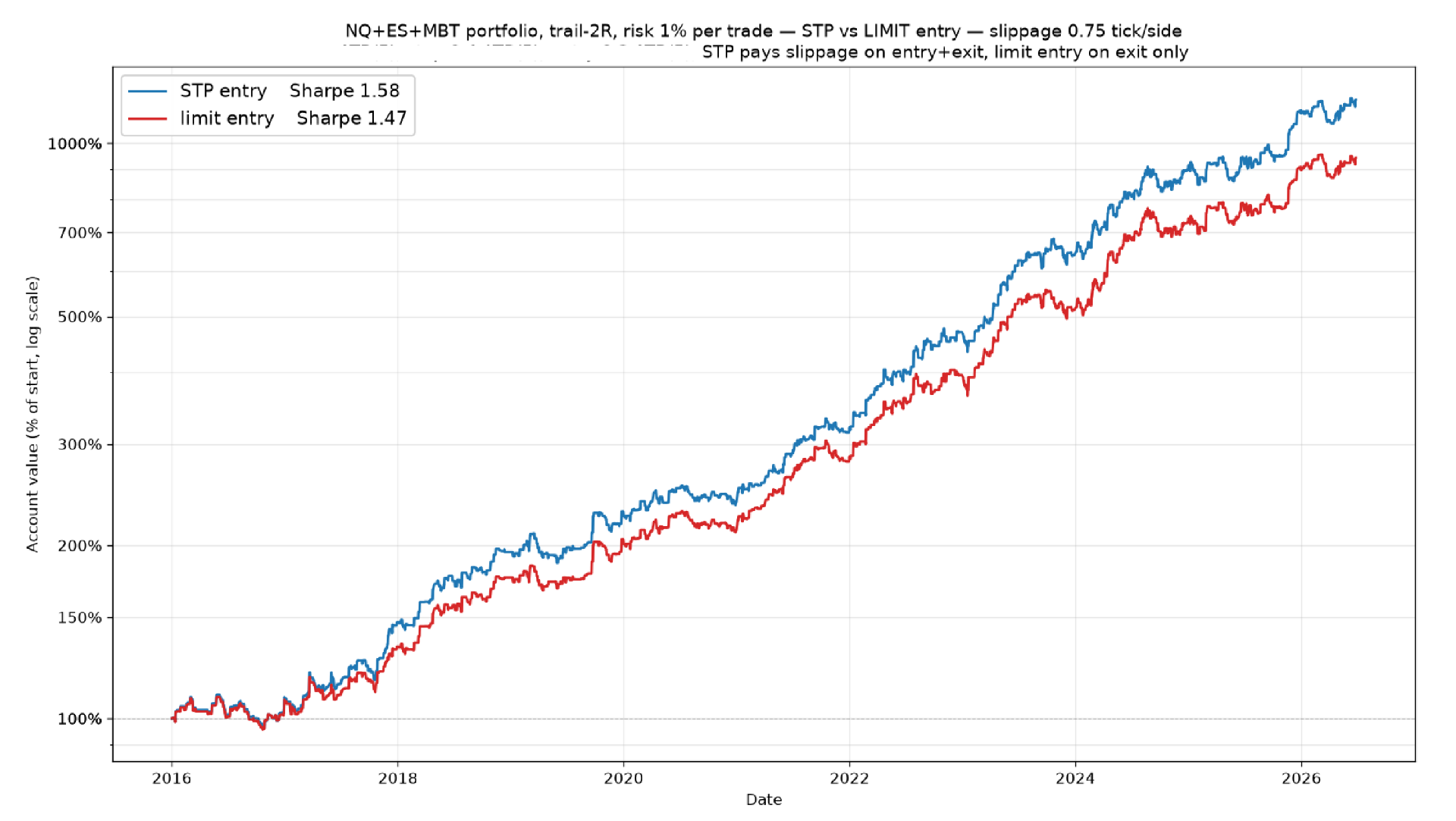

Figure 3 shows the comparison when I assume relatively low slippage: 0.75 tick per side.

At low slippage, the stop entry still wins. The advantage of being in the trade earlier is larger than the execution saving from the delayed limit order.

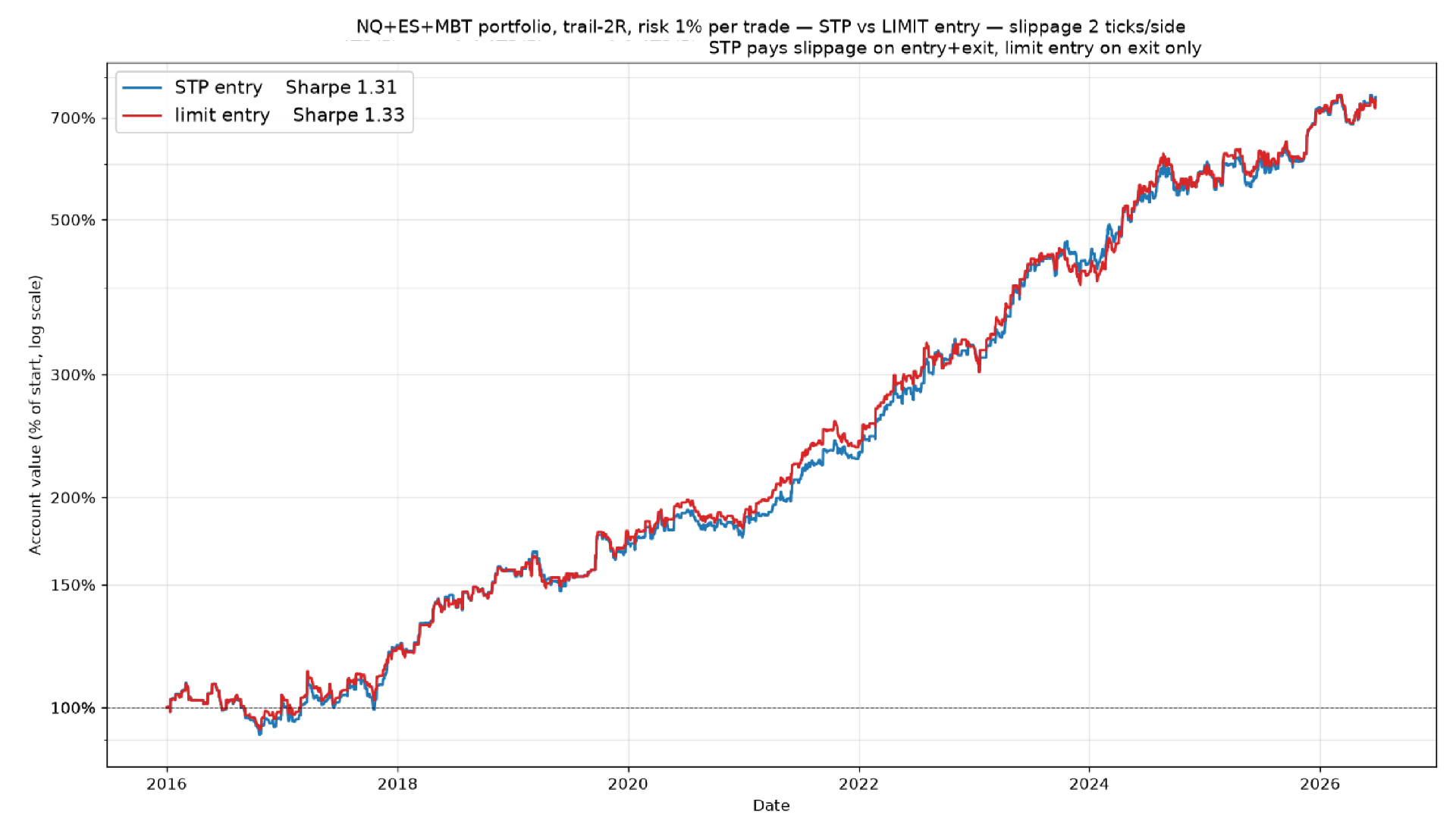

But when I increase the assumed slippage to 2 ticks per side, the picture changes.

This is useful information. It tells me two things.

First, the breakout edge is strong enough to absorb even higher slippage assumptions. That is good news.

Second, delayed limit entry is a valid execution path. It may be especially useful when trading larger positions, less efficient instruments, or instruments where market orders are simply too expensive.

This is also where the research becomes especially useful for options.

Why 0DTE options fit intraday breakouts

As I have shared on X and in live updates, I also trade the breakout idea using long 0DTE options. 0DTE means zero days to expiration. These are options that expire on the same day.

At first, I test/trade this in a very naive way. When the underlying market broke the breakout level, my bot bought an in-the-money call or put option using a market order.

That is not an elegant execution model. The slippage can be significant.

And yet, even this simple version has produced strong results on a dedicated live account, as shown in Figure 5.

The reason 0DTE options fit breakout trading is clear.

With a long option, the maximum loss is the premium paid. We do not need a traditional stop-loss on the underlying position because the position cannot lose more than the option premium.

At the same time, if we catch a strong trend day and hold the option into the close, the convexity of the option can work strongly in our favor.

This is exactly what an intraday breakout system is trying to do: survive many small failed moves and participate aggressively in the few large directional days.

The biggest challenge is execution.

Buying 0DTE options with market orders at the breakout can be expensive. The bid-ask spread is wider than in SPY or QQQ shares, and the option price can move very quickly.

This is where the delayed limit entry tested above becomes useful.

Applying delayed limit entries to 0DTE options

Instead of buying the 0DTE option immediately with a market order at the breakout, we can use a more controlled process:

- wait for the underlying to close a one-minute bar beyond the breakout level,

- select the appropriate in-the-money call or put,

- place a limit order based on the option price at the signal bar,

- if it is not filled within one minute, move the limit to a new price based on the option price at the close of the last 1-minute bar.

- hold the option until the end of the day.

Figure 6 compares ETF breakout trading with 0DTE option breakout trading in the period where 0DTE data is available. The option results include realistic fees and slippage assumptions.

The ETF version remains cleaner and more direct. But the 0DTE version requires much less capital because we only need to pay the option premium. Depending on the symbol, strike, volatility, and time of day, this can be only a few hundred dollars per contract.

That makes 0DTE options very interesting for a breakout portfolio.

They are interesting because they express the same edge in a different way:

- limited risk through the paid premium,

- stronger convexity on trend days,

- no need to use a stop loss, and the position thus survives bigger pullbacks,

- potentially lower capital requirement,

My current direction

Based on these tests, I am starting to combine two variants of the same intraday breakout idea.

The first variant is for ETFs and micro futures:

2R delayed trailing stop

This is psychologically easier than the pure fixed exit. The trade still has enough room to develop, but once it has produced meaningful open profit, part of that profit is protected.

The second variant is for 0DTE options:

fixed exit via 0DTE, delayed limit entry, and hold to end of day.

This variant is designed to target the strongest trend days, which the 2R delayed trailing stop does not always catch. The option premium defines the maximum loss, and the end-of-day hold allows the option convexity to work when the market really expands.

I plan to allocate the risk budget roughly 50/50 between these two ideas.

This is also a good way to reduce dependence on one execution method.

Final thoughts

The main lesson from this research is simple:

a trading edge is not just an entry signal.

It is the full process around the signal.

For intraday breakouts, the entry logic can be very simple. But live results depend on the details.

The fixed exit remains one of the strongest and most robust ways to trade intraday breakouts. But the 2R delayed trailing model may be easier to trade live. Delayed limit entries may help when slippage becomes too expensive. And 0DTE options offer a capital-efficient way to express the same breakout idea with capped premium risk and strong trend-day convexity.

After I finish deeper live testing, I will share the updated IBKR tools with traders who joined my implementation program. The updated tools will support both trailing stop management and 0DTE option execution using limit orders.